Uber: The Everything Platform That Still Has Something to Prove

From Austin rideshares to Osaka pharmacies to Waymo robotaxis, Uber is everywhere. The question is whether everywhere is enough.

Last November, a woman in Austin opened the Uber app to refill a prescription. Not to hail a ride to the pharmacy, but to have the medication delivered to her door. The order was picked up by a driver who, thirty minutes earlier, had dropped off a passenger at the airport and, thirty minutes later, would deliver Thai food across town. Three transactions, three business models, one platform, one driver. Down the street, a Waymo robotaxi completed a ride booked through that same Uber app, with no driver at all.

That single Austin afternoon captures both the ambition and the tension defining Uber in April 2026. The company is no longer just a rideshare app. It is a logistics network that processes $193 billion in gross bookings annually, in variations that range from airport rides in Tokyo to grocery runs in London to a restaurant in Mexico City paying for a top search placement so its tacos show up first on Uber Eats. The question for investors is not whether Uber is big. It is whether Uber can remain the indispensable layer between supply and demand when the supply itself is being reinvented by machines.

The Business: Three Segments, One Network

Uber operates three segments, but two of them carry almost all the weight.

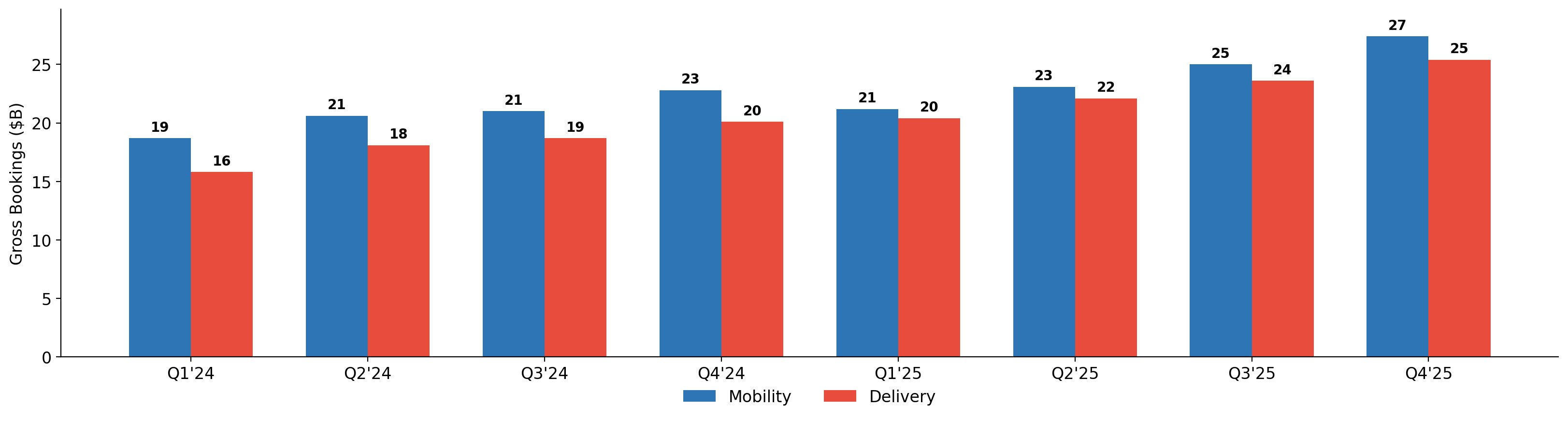

Mobility is the original rideshare business. Per Uber’s FY2025 filing, it generated $29.7 billion in revenue, up 18% year over year, and represented 57% of total company revenue. Uber commands roughly 74% of U.S. rideshare spending, according to Bloomberg Second Measure, with Lyft holding the remainder. That dominance is structural: drivers earn more on Uber because rider density is higher, and riders get faster pickups because driver supply is deeper. This is a classic two-sided network effect, and it gets stronger as the platform scales. Lyft’s best year of revenue growth in 2024 (31% to $5.8 billion) still left it at roughly one-fifth of Uber’s mobility revenue, underscoring how difficult it is to close the gap once network effects compound.

Delivery is the growth engine. Revenue reached $17.2 billion in FY2025, up 25% year over year, making it the fastest-growing segment. Delivery gross bookings grew 26% in Q4 alone, accelerating from 18% growth in Q1. What started as restaurant food delivery now includes groceries, convenience items, alcohol, and prescriptions. The segment shares drivers with Mobility, which means incremental deliveries can be fulfilled at lower marginal cost. Uber One, the company’s membership program, is the connective tissue: members who use both rides and delivery spend and order more frequently, creating a self-reinforcing loop.

Freight generated $5.1 billion in revenue, essentially flat year over year, and operates in a structurally different market. It is a digital brokerage matching shippers with carriers, and the freight market has been in a prolonged downcycle since 2022. Analysts at Bloomberg and FreightWaves have periodically speculated about a potential spin-off or sale of the unit. For now, Uber is investing in last-mile capabilities and aims to cover 85% of the U.S. population by the end of 2026. Freight is a non-material contributor to the investment thesis today, and this analysis will focus on Mobility and Delivery.

The Financial Machine

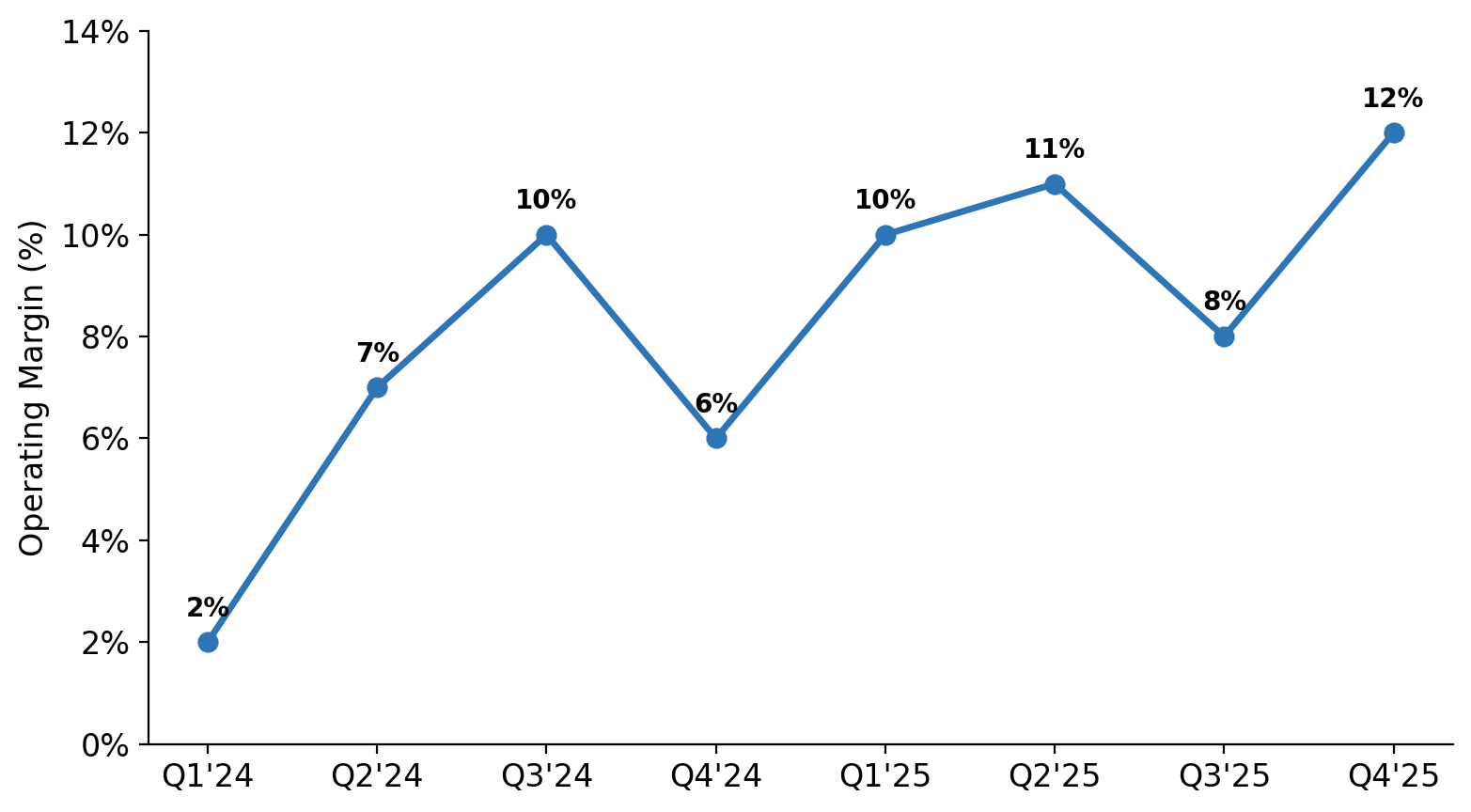

Uber’s FY2025 results marked a company that has crossed from growth-stage economics into mature platform profitability. Total revenue reached $52 billion, up 18% year over year, according to the company’s annual filing.

The profitability trajectory is the more important story. GAAP operating income hit $5.6 billion, roughly doubling from the prior year and producing an operating margin above 10%. Two years ago, the company was barely profitable on a GAAP basis.

The operating leverage behind that expansion is structural: each incremental ride or delivery order flows through an existing network of drivers, merchants, and software infrastructure, and the cost to serve that order grows much more slowly than the revenue it produces.

Marketing efficiency has improved dramatically. Uber’s advertising business, which lets restaurants and brands pay for promoted placements on the app, surpassed a $2 billion annualised run rate per the company’s Q4 2025 earnings report, growing over 50% year over year. This is nearly pure-margin revenue: it requires no incremental driver supply or delivery logistics, and it subsidises the cost of acquiring and retaining users. The broader pattern is that each new monetisation layer, advertising, membership, and financial services, extracts more value from the same underlying transaction volume.

On capital allocation, Uber announced a $20 billion share buyback authorisation in August 2025, supplementing its earlier program from 2024. CFO Prashanth Mahendra-Rajah has stated that at least half of the company’s cash flow will be used for repurchases, suggesting the pace will accelerate.

The valuation today sits at approximately 22x trailing adjusted EBITDA ($8.7 billion in FY2025), according to GuruFocus as of early April 2026. That multiple compresses meaningfully on forward numbers: management guided Q1 2026 adjusted EBITDA of $2.37 to $2.47 billion, implying a full-year 2026 run rate north of $10 billion. At the current enterprise value of roughly $155 billion, that would put the forward multiple closer to 15x. For a company growing gross bookings 17 to 21% and generating nearly $10 billion in annual free cash flow, that compares favourably to DoorDash (which trades at higher revenue multiples with lower margins) and to the broader market.

Uber One and the Membership Moat

The most underappreciated asset in Uber’s portfolio may be its membership program. Uber One reached 46 million members by the end of FY2025, growing 55% year over year. That scale matters because membership programs fundamentally change the economics of a marketplace: they reduce churn, increase order frequency, and make the platform the default rather than a choice that gets re-evaluated each time.

Per the company’s FY2025 earnings materials, Uber One members now account for roughly 50% of gross bookings. When half of all transaction volume flows through a membership layer, the platform becomes structurally stickier, and competitors must overcome both habit and sunk cost to poach users.

Anecdotally, Uber One members use both Mobility and Delivery at higher rates than non-members, and the cross-platform stickiness is the most structurally valuable outcome. A rider who also orders groceries through Uber is far less likely to switch to Lyft for rides or DoorDash for food. The $9.99 monthly fee is a sunk cost that nudges behaviour toward consolidation on a single platform, the same psychological mechanic that makes Amazon Prime so durable. In the delivery market specifically, Uber Eats, without an Uber One membership, is more expensive than DoorDash on a per-order basis. With Uber One, pricing becomes competitive, making the membership program not just a retention tool but also a pricing equalisation mechanism that keeps Uber Eats viable against a dominant competitor.

The Delivery Race Is Not Over

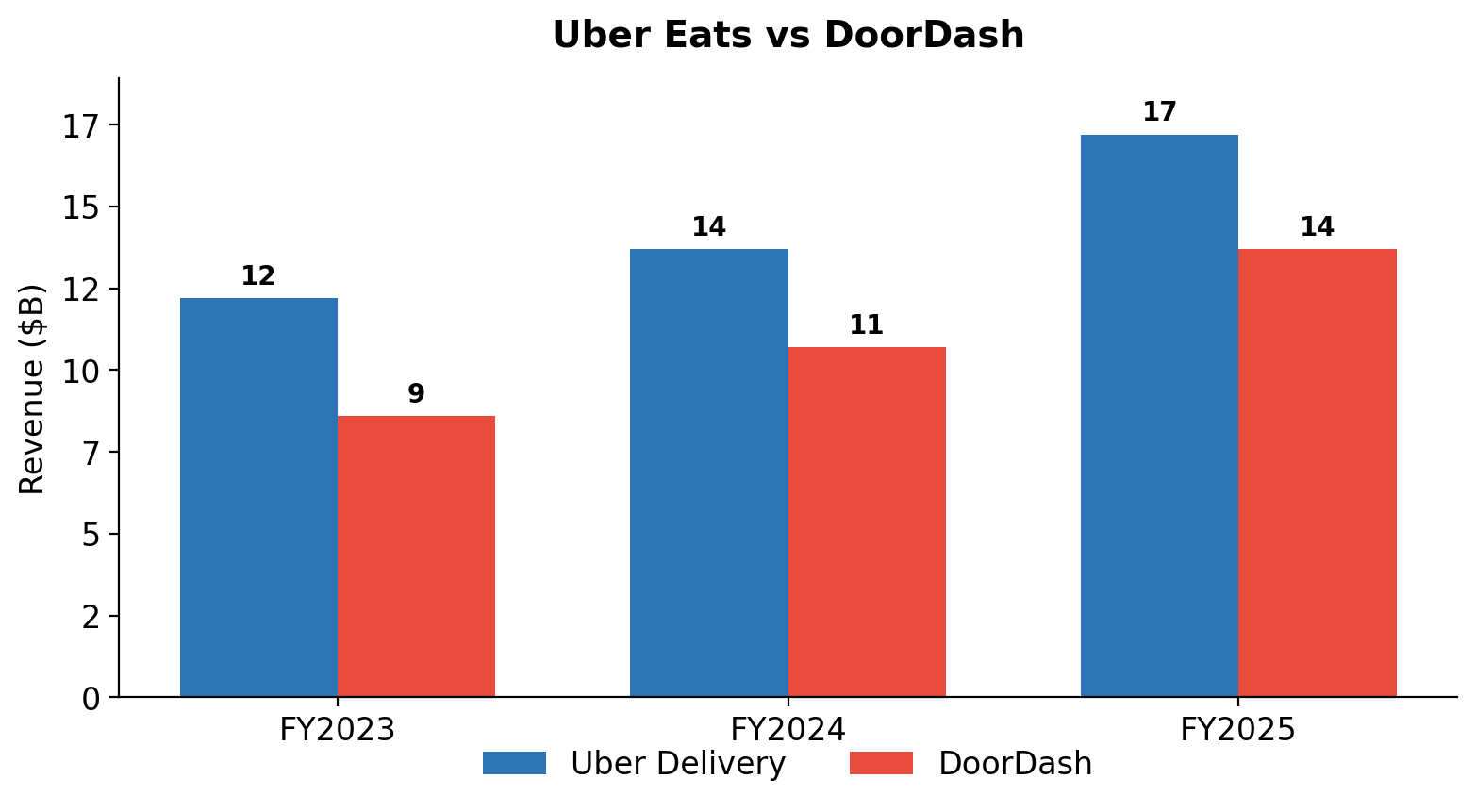

Uber’s delivery business is growing fast, but it is not winning market share in the United States. According to Bloomberg Second Measure data for early 2026, DoorDash commands approximately 60% of U.S. food delivery spending, with Uber Eats at roughly 23% and Grubhub trailing in the single digits to mid-teens, depending on methodology.

DoorDash’s FY2025 revenue reached $13.7 billion, up 28% year over year, and the company is now GAAP profitable with a 5.3% operating margin. This is not a competitor in retreat.

The competitive dynamic comes down to where each platform is strongest. DoorDash is delivery-first: it has the deepest restaurant and merchant network in the U.S., particularly in suburbs and smaller cities where selection matters most. Its DashPass membership program has strong retention, and in many U.S. markets, it delivers faster than Uber Eats. Consumers who prioritise restaurant variety and speed tend to default to DoorDash.

Uber’s advantage is cross-platform density and promotions. A driver completing a ride can immediately pick up a food delivery; a user opening the app for a ride sees a prompt to order dinner. This shared infrastructure means Uber can serve delivery at a lower incremental cost, even if DoorDash has a higher delivery-specific market share. Uber Eats also tends to offer more aggressive coupons and promotions, particularly to new users, and the Uber One cross-segment value proposition (rides plus food plus groceries for one membership fee) has no DoorDash equivalent.

Internationally, Uber has historically held the advantage, with meaningful delivery scale in Latin America, Europe, and parts of Asia where DoorDash had limited or no presence. That picture shifted in late 2025, when DoorDash acquired Deliveroo for approximately $3.9 billion, expanding its reach to over 40 countries and an addressable population of over 1 billion people. DoorDash now has meaningful scale in the UK, France, Italy, Singapore, and the Middle East, markets where Uber previously competed against smaller local players rather than a well-funded global rival.

The Deliveroo acquisition does not erase Uber’s international position, but it narrows the gap. Much of the 26% Q4 delivery gross bookings growth came from international markets, and Uber retains structural advantages in Latin America and parts of Asia where DoorDash still lacks presence. The stabilisation at 23% U.S. share despite DoorDash’s growth suggests that Uber One and international expansion are providing enough ballast to hold position domestically, even as the international delivery race becomes more contested.

But the competitive threat Uber faces is not limited to the delivery wars.

Autonomous Vehicles: The Defining Question

The single biggest structural question for Uber over the next decade is whether autonomous vehicles will strengthen or dismantle its business model. The answer is not obvious, and both scenarios are genuinely plausible.

The threat is straightforward. Uber’s current model relies on human drivers, and the company’s largest expense is the share of each fare paid to them. If a competitor can deploy autonomous vehicles at scale and distribute rides on its own app, it could offer rides at a fraction of Uber’s cost while keeping the entire fare. Waymo, owned by Alphabet, is the only AV company operating at a meaningful scale today. It runs approximately 3,000 vehicles across ten U.S. metro areas, completed over 500,000 weekly rides as of March 2026, and aims to reach one million weekly rides by the end of the year. In San Francisco, Waymo has been gaining market share from Uber, though Uber’s total share of the city’s rideshare market remains much larger.

The tier below Waymo is smaller and moving more slowly than headlines suggest. Tesla launched an unsupervised Model Y robotaxi service in Austin on June 22, 2025, with approximately 10 vehicles initially. As of April 2026, the fleet has grown to roughly 40 vehicles in Austin, well behind Elon Musk’s original target of 500, which he slashed to approximately 60. Tesla has been spotted testing in Phoenix but has not launched commercially outside Austin. Separately, Tesla’s purpose-built Cybercab, a vehicle with no steering wheel designed from the ground up for autonomous operation, began early production at Giga Texas in April 2026 but has not yet entered passenger service. Tesla’s autonomous ambition is real, and its manufacturing scale remains a long-term structural advantage: if the software matures, the Cybercab gives Tesla a cost-per-mile edge that no retrofitted vehicle can match. But execution is far behind Waymo, and investors should weigh actual fleet size over forward projections. Amazon’s Zoox began offering driverless rides around the Las Vegas Strip and parts of San Francisco.

The production bottleneck matters. Even Waymo, the clear leader, faces a hard growth ceiling. Its new Arizona factory, built in partnership with manufacturer Magna (using Hyundai’s Ioniq 5 as the vehicle platform), can produce tens of thousands of vehicles per year, though current output remains well below that ceiling. That is a fraction of what would be needed for national coverage. By contrast, Uber has millions of human drivers who can scale immediately to any neighbourhood, suburb, or secondary city. Waymo’s current service areas do not extend to suburbs in most cities, a major limitation given that suburban trips represent a large share of rideshare demand. When it rains heavily, when roads are icy, when a fallen tree blocks a route, or when police redirect traffic at an accident scene, autonomous vehicles underperform or cannot operate at all. A pure AV app simply shows no rides available. Uber’s mixed model, humans plus machines, provides redundancy that no single-technology fleet can match.

Uber’s counter-strategy has been to position itself as the demand platform that AV companies need. The logic: building autonomous driving technology is extraordinarily expensive, but distributing autonomous rides at scale, routing them efficiently, managing surge pricing, and handling customer service are different kinds of hard problems that Uber has already solved. CEO Dara Khosrowshahi noted on the Q4 2025 earnings call that Waymo vehicles on Uber’s platform are “busier than 99% of our drivers” in markets like Atlanta and Austin, because Uber’s demand density keeps them constantly occupied. On Waymo’s own app in San Francisco and Phoenix, utilisation is structurally weaker because Waymo lacks a comparable demand routing system. That utilisation gap is Uber’s strongest argument for why AV companies will route through its platform rather than go it alone.

Early data from Austin illustrates the emerging competitive landscape. Tesla’s Model Y robotaxis are the cheapest option per mile, though availability remains limited while the fleet scales. Waymo rides booked through Uber sit in the mid-price tier. Human Uber drivers are the most expensive per trip but the most available.

Early user surveys suggest that trust and perceived safety matter more than price for robotaxi passengers, with riders willing to pay a premium for Waymo over Tesla due to Waymo’s longer track record. This is a dynamic that favours established AV operators, and by extension, favours a platform like Uber that can offer riders the choice.

The Waymo Partnership: Powerful but Fragile

The Uber-Waymo relationship deserves close scrutiny because it is structured on a city-by-city basis and is not permanent. In Austin and Atlanta, Uber is Waymo’s exclusive rideshare partner. In San Francisco, Phoenix, and Los Angeles, Waymo operates its own consumer app in parallel with Uber integration. Many analysts expect Waymo to exit its exclusive markets once it has built sufficient brand awareness and rider habits, potentially by late 2026 or 2027.

That exit risk is real, but Waymo’s production constraints limit how quickly it can go independent at scale. With approximately 3,000 vehicles U.S.-wide and factory output still ramping, Waymo cannot saturate even one major metro area on its own, let alone cover the national footprint that Uber’s millions of human drivers already serve. The math favours Uber’s multi-AV strategy for the medium term: by partnering with Waymo, Zoox, and others simultaneously, Uber avoids dependence on any single manufacturer and can offer riders the broadest selection of autonomous options.

The long-term vision, which is not yet at scale, is closer to a marketplace: multiple AV providers listed on the Uber app, with the algorithm assigning the best vehicle based on price, wait time, and rider preferences. If that marketplace materialises, Uber’s take rate could actually increase as AV providers compete for demand allocation, much like hotels competing for placement on Booking.com.

The Rivian Bet: Hardware Without Proven Software

Uber’s $1.25 billion partnership with Rivian, announced in March 2026, represents a different kind of AV bet. Rivian is not an autonomous vehicle company. It is an electric vehicle manufacturer, best known for building over 100,000 Amazon delivery vans. The R2 model that Uber will deploy is designed as an autonomous vehicle from the ground up, with a lower trunk built for camera arrays and the option to remove the steering wheel entirely.

The deal structure calls for up to 50,000 custom-built R2 robotaxis across 25 cities in the U.S., Canada, and Europe by 2031, with an initial $300 million investment and the first vehicles expected in San Francisco and Miami in 2028. Uber brings the demand network and routing intelligence. Rivian brings both the physical vehicle and the autonomous driving software: in December 2025, Rivian announced its third-generation autonomy platform, featuring 11 cameras, 5 radars, LiDAR, and in-house RAP1 compute chips.

The risk is execution, not sourcing. Rivian is building its AV stack in-house, but it has not yet demonstrated the capability needed for unsupervised autonomous driving. The $1.25 billion bet assumes Rivian’s software reaches that quality bar by 2028. If it does not, Uber has a fleet of expensive electric vehicles with no autonomy. If it works, Uber has a proprietary fleet with economics it controls directly, bypassing the take-rate negotiations it faces with Waymo and Zoox.

The Labour Model Shapes the AV Transition

There is a strategic dimension to the autonomous vehicle transition that rarely appears in investor presentations: the regulatory classification of drivers determines how quickly a company can shift from human to machine labour.

In the United States, Uber’s drivers are independent contractors, protected by California’s Proposition 22 and similar frameworks. This is Uber’s most important regulatory shield, not just for current economics but for the AV transition itself. With contractors, Uber can gradually route more trips to autonomous vehicles and fewer to human drivers. Contractors who earn less simply drive less or leave the platform. There are no severance obligations, no social plans, and no works council negotiations.

The picture is very different in markets with employment mandates. In the United Kingdom, a 2021 Supreme Court ruling classified drivers as “workers” entitled to minimum wage, holiday pay, and pension contributions. Uber complied. In Spain, the 2021 “Ley Rider” law mandated employment of delivery drivers; Uber Eats initially withdrew from the market and returned with a subcontractor model that preserved flexibility.

The EU Platform Work Directive, which member states must transpose into national law by late 2026, could accelerate this trend across the entire European Union, potentially forcing reclassification in markets where Uber currently uses contractor or subcontractor models.

The strategic implication is underappreciated. In countries where drivers are employees, the AV transition creates a restructuring problem. If Uber has tens of thousands of employed drivers in Germany and autonomous vehicles arrive, it faces social plans, severance costs, works council negotiations, and political backlash. The cost of reducing headcount could exceed the savings from autonomous vehicles for years. This suggests that the AV rollout will be fastest in the U.S. (contractor model), slowest in the UK and Continental Europe (employment mandates), and intermediate in markets where Uber has adopted the Spanish subcontractor model. Investors modelling a uniform global AV transition are likely overestimating near-term margin expansion in regulated labour markets.

The International AV Opportunity

Internationally, the autonomous vehicle landscape is fragmented in ways that could favour Uber. China is effectively a walled garden: Baidu Apollo and Pony.ai dominate, and Western platforms have no meaningful presence. That market is lost to Uber.

Europe and Latin America, however, have virtually no autonomous robotaxi offerings today. Uber already operates the demand network in these regions. If it can onboard AV vehicles from various manufacturers, whether the Rivian R2, a future Waymo international expansion, or regional AV developers, it could be the first mover for autonomous rides outside the U.S. and China. The demand side of the equation is already built. The supply side is what needs to arrive.

Macro Headwinds Worth Watching

Uber’s business is largely driven by domestic services, which insulates it from tariff risk on physical goods. You do not pay import duties on a rideshare trip. But the 2026 macro environment creates indirect headwinds worth naming.

Regulatory risk is intensifying on multiple fronts. The FTC has been probing Uber over deceptive earnings claims and potential antitrust violations, including alleged coordination with Lyft to suppress driver pay in New York City. If the probe results in enforcement action, it could produce fines, behavioural remedies, or restrictions on pricing practices.

More directly relevant to the investment thesis, the FTC and 21 state attorneys general filed an amended complaint in December 2025 alleging that Uber enrolled consumers in Uber One without clear consent, promised savings that did not materialise, and made cancellation deliberately difficult, requiring up to 32 actions across as many as 23 screens. Given that Uber One members now account for roughly half of all gross bookings, a legal challenge targeting the program’s enrollment and retention mechanics poses a material risk to one of the company’s most important competitive advantages.

Separately, the EU Platform Work Directive, which member states must transpose into national law by late 2026, could force reclassification of gig workers as employees across the European Union. The directive is broader and more prescriptive than the UK and Spain rulings that the company has already navigated. If applied strictly, it would increase Uber’s cost structure in its second-largest market and slow the AV transition in Europe by creating employment obligations that are expensive to unwind. On a parallel track, the EU AI Act takes effect on August 2, 2026, and Uber’s matching, dynamic pricing, and driver management algorithms could face scrutiny as high-risk AI systems, with fines up to 3% of global annual turnover for high-risk AI non-compliance.

Beyond currency and regulation, the broader macro picture introduces uncertainty. Consumer spending has remained resilient through early 2026, but softer labour markets and tariff-driven price increases on goods could squeeze discretionary budgets. Rideshare and food delivery are not pure necessities. A household cutting expenses might consolidate restaurant orders or choose public transit over an Uber. The magnitude of this risk is hard to quantify, but it is the kind of environment where investors should expect growth deceleration rather than acceleration.

Scenario Analysis

🔴 Bear Case: The Platform Gets Bypassed

5-year outlook: Revenue CAGR 5% to 8% | Operating Margin 8% to 10%

In this scenario, Waymo accelerates production through new manufacturing partnerships and distributes rides primarily on its own app, eroding Uber’s rideshare dominance in major U.S. cities over three to five years. Tesla leverages its manufacturing advantage to scale the Cybercab from hundreds to tens of thousands of vehicles, undercutting Uber on price in sunbelt cities with predictable weather. Uber retains a role as one distribution channel among many, but its take rate compresses as AV companies gain leverage and exit exclusive agreements. DoorDash extends its U.S. delivery lead and leverages the Deliveroo acquisition to challenge Uber in European and Middle Eastern markets, pressuring Uber’s delivery margins on both fronts. Employment mandates in Europe slow the AV transition there while competitors capture the U.S. market. Rivian’s in-house AV software fails to reach unsupervised driving capability by 2028, stranding Uber’s $1.25 billion investment. Macro headwinds dent rideshare frequency in 2026 and 2027. Uber remains profitable but grows at a fraction of its current pace, and the stock re-rates to a utility-like multiple.

🟡 Base Case: The Compounding Continues

5-year outlook: Revenue CAGR 12% to 15% | Operating Margin 12% to 15%

Uber’s platform strategy works as designed. Waymo’s production bottleneck limits its ability to operate fully independently, and it continues to route through Uber in most cities even as it operates its own app in a handful of metros. Tesla’s Cybercab grows to several thousand vehicles by 2027 but remains sub-scale relative to national rideshare demand through 2028. The Rivian fleet begins deploying in 2028 with functional in-house AV software, adding a proprietary margin layer in select cities. Delivery grows at a mid-teens annual rate as international markets mature and advertising revenue scales toward 4 - 5 billion. Uber One membership surpasses 80 million, deepening cross-platform engagement and keeping Uber Eats competitive against DoorDash despite its domestic lead. The U.S. contractor model enables fast AV integration; European markets lag by two to three years due to labour regulations. Operating margins expand as the mix of advertising and membership revenue shifts upward. The buyback program shrinks shares by 3 to 4% annually, compounding EPS growth beyond revenue growth. The stock trades at 18 to 22x forward EBITDA, reflecting a mature platform compounder.

🟢 Bull Case: The Autonomous Marketplace

5-year outlook: Revenue CAGR 18% to 22% | Operating Margin 16% to 20%

Uber becomes the default marketplace for autonomous mobility globally. Multiple AV providers, Waymo, Zoox, Rivian-powered vehicles, and regional manufacturers all route through Uber because its demand density delivers utilisation rates no standalone app can match. The Uber app evolves into a marketplace where riders choose between AV options by price, wait time, and safety rating, and AV companies bid for demand allocation, pushing Uber’s effective take rate higher. The Rivian partnership scales ahead of schedule, and Uber’s first-mover advantage in European and Latin American AV deployment opens markets that pure AV companies cannot yet reach. Weather-related AV limitations make the mixed human-plus-machine model a lasting structural advantage rather than a transitional one. Advertising becomes a $7 to 10 billion business as the platform’s data advantages compound. Uber One exceeds 100 million members. Operating margins approach 20% as autonomous rides eliminate driver payouts on a growing share of trips. The stock re-rates to a premium platform multiple.

What to Watch

Waymo’s exclusive market behaviour: If Waymo launches its own consumer app in Austin or Atlanta before the end of 2026, it signals the exclusive partnership is fraying. If Waymo stays exclusive, it validates Uber’s utilisation advantage.

AV ride volume on Uber’s platform: Uber has stated it aims to offer driverless rides in 15 cities by the end of 2026. Track the number of cities and the weekly ride volume. This is the most direct measure of whether the platform strategy is working.

Delivery gross bookings growth vs DoorDash: Track the relative growth rates each quarter. Uber holding at 23% U.S. share while growing internationally signals the duopoly is stable. Uber’s share dropping below 20% would suggest DoorDash is pulling away decisively.

Rivian AV software milestones: Rivian is developing its autonomy stack in-house, so the key question is whether the software reaches unsupervised driving capability on schedule. Track public testing milestones and any regulatory approvals. A significant delay past mid-2027 would materially change the risk profile of the $1.25 billion deal.

Free cash flow conversion: FCF of $10 billion on $5.6 billion operating income reflects a highly capital-efficient model. If FCF growth stalls while operating income grows, it may signal increased capex demands from the Rivian fleet investment or other AV commitments.

European labour model evolution: Watch for Uber shifting more markets toward the Spanish subcontractor model. That would signal the company is proactively clearing the path for AV deployment in regulated labour markets.

Final Verdict

Uber is a hold for existing investors and a reasonable entry for new capital on pullbacks below 18x forward EBITDA. The business has crossed a profitability inflection that the market has not fully priced in, and the AV landscape is evolving in ways that favour a platform aggregator over the next three to five years, primarily because no AV company can produce enough vehicles to go it alone at a national scale.

The conditions that would flip this to a strong buy: Rivian demonstrates unsupervised driving capability with its in-house AV stack, and Waymo renews its exclusive agreements in Austin and Atlanta beyond 2026. The condition that would flip it to a sell: Waymo or Tesla reaching 10 million weekly rides on their own apps without Uber, signalling the platform is being bypassed.

Better information, sharper decisions ✌️